The Corrupt System Behind Covid Medical Shortages

The Corrupt System Behind Covid Medical Shortages

Why are we still facing shortages of masks and medicine a year and a half after the start of the pandemic? Because a buying cartel controls medical supplies, and has for 25 years.

Hi,

Welcome to BIG, a newsletter about the politics of monopoly. If you’d like to sign up, you can do so here. Or just read on…

Over the past few weeks, I’ve been writing about shortages, and getting a lot of feedback. One of the most common complaints I’m hearing is from medical personnel, who tell me about shortages in everything from masks to blue top collection tubes used to test blood clotting to lidocaine to gloves. There’s a well-known set of monopolies behind this problem, so that’s what I’m writing about today.

Plus:

How the Federal Reserve Caused a Massive Merger Wave

Lina Khan Lays Out Priorities for an Overwhelmed FTC

Did Mark Zuckerberg Engage in Insider Trading?

First, some house-keeping. I was on the podcast RealVision with financial expert Mike Green, which you can watch here. And now…

Shortages Aren’t New

Today, with supply chains tangled in knots and shortages everywhere in the economy, it’s easy to blame what’s gone wrong merely on the disruptions caused by Covid. Indeed, David Frum at the Atlantic is the latest to mock the idea that there is something wrong with our markets that set us up with a fragile system. Frum criticized the new approach to concentration as taking us back to the 1970s. Pursuing ‘resiliency’ translates in “plainer English as higher taxes and higher prices.” Instead, he suggests that we should, in the face of inflation and shortages, “do nothing,” because the immutable laws of supply and demand will work themselves out.

There are a couple of reasons that dismissive attitude doesn’t make sense. Health care is a great place to understand problems with supply chains, because they predate Covid by 20 years. For more than 10 years, hundreds of drugs or medical supplies – everything from saline to epinephrine to chemotherapeutic agents to antibiotics, to sterilized water - have been regularly in short supply or outright shortage. The shortage problem is clearly not due to Covid, though Covid exacerbated it.

This became clear when I got feedback from you on the shortages you’re seeing. Doctors told me that they often have to switch from drugs they understand to lesser known drugs because of shortages, which can lead to medical errors, but that this situation isn’t a result of Covid. In fact the FDA has had a drug shortage webpage for years.

Here’s one reader making the point.

New shortages cropping up all the time in healthcare. I first noticed it around 2017-2018 after a storm affected production of saline in Puerto Rico. This limited supplies of fluid for intravenous infusion. Ever since then, especially after the Covid 19 pandemic hit, an unpredictable shortage will hit the hospital where I work. Right now, there’s a lidocaine shortage. Before that, it was the gloves we would normally use, which were replaced with whatever the hospital could get it’s hands on, the worst being flimsy ones from Malaysia that clearly hadn’t gone through quality control because they would stick together in the box and rip when you tried to put them on, wasting half the box. Before that it was opioid pain medication, medications to sedate and/or paralyze patients on ventilators, N95 masks, and respirators. It always seems as if you solve one issue, and another crops up to replace it.

Shortages of medicine and personal protective equipment, while understandable the beginning of the pandemic, make little sense eighteen months later. Early last year, large numbers of domestic firms that produce textiles retooled to produce PPE, material like meltblown for masks. We now have an industry that can make a lot of different medical supplies, though clearly not everything. But what I’m told is that the domestic supply chain, while now impressive, simply cannot sell into domestic hospitals. And that means these new firms are going to stop investing and shut down what they are producing. This is a profoundly weird situation. If there are shortages, why can’t hospitals buy from new producers?

The story always seems to come back to changes in hospital buying that took place thirty years ago, among a small group of middlemen known as Group Purchasing Organizations, or GPOs.

You Be Sure and Thank Masie for This Fine Pie

In 1993, just after the end of the Cold War, American doctors noticed something new and disturbing about the U.S. medical system. The Soviet Union had collapsed, in part due to a dysfunctional economic system that couldn’t deliver basic goods. By contrast, the United States was known for having a world-class, domestic, and resilient supply chain for important goods, like medicines. But that year, three serious nationwide shortages occurred in the U.S. in quick succession, for drugs to treat AIDS, tuberculosis, and heart conditions.

It was something of a shock, and the New York Times went digging, finding the problem was rooted in monopoly production. “Many drugs are made by only one company,” reported the paper, so “a serious manufacturing or financial problem could leave the United States vulnerable to a sudden disruption in the supply of a standard drug.” This wasn’t supposed to happen in the land of supply and demand. Higher demand for certain products should have led to higher prices and then more supply, which is how markets are supposed to work. Shortages didn’t figure in the picture. Still, it seemed to be a one-off.

In 1999, there was another shortage, this one of something much more basic: penicillin. Again the culprit was concentrated production. A factory run by Marsam Pharmaceuticals that produced 60% of the penicillin G used in the U.S. shut down after the government found serious production deficiencies. A few years later, shortages had become routine. Prices for medicines or medical devices and material might go up, hospitals would want to buy, but new supply wouldn’t come online. In 2001, one hospital executive observed publicly, “Something strange is going on.”

From roughly 2000-2006, business journalists and policymakers began delving into what was happening in the medical and drug supply chains, unmasking a set of middlemen, known as Group Purchasing Organizations (GPOs), who had cartelized the hospital purchasing market. The New York Times did a series called Medicine’s Middlemen. The Senate soon held hearings, and government investigators began looking into the industry. What they found was disturbing.

GPOs are buying coops for hospitals, a kind of Costco or Sam’s Club for all sorts of medical supplies and medicines, with hospitals as the members. The first was started in 1910, and until the 1980s, GPOs served as ways for hospitals to get a wide selection of products at volume discounts. But in 1987, under pressure from hospital lobbyists, Congress loosened anti-kickback laws that prohibited GPOs from taking fees from vendors. This shift, which went into effect in 1991, radically changed the industry, and explains why supply and demand signals stopped working.

Prior to the legalization of kickbacks, GPOs were basically just catalogues of supplies, matching hospitals with suppliers and serving a basic market-making function. Soon that changed. GPOs, which had been financed by hospital members, were now financed by the suppliers they were supposed to be negotiating with for lower prices. As Phillip Zweig wrote:

After the GPO safe harbor rules were implemented in 1991, GPOs no longer cared about saving hospitals money. Their goal now was to maximize fee (a.k.a kickback) revenue. And because GPO fees are based on a percentage of sales volume, the higher the price of hospital supplies, the more fees GPOs collect. These perverse incentives gave rise to a system in which vendors compete for exclusive GPO contracts based not on who can supply the best product at the best price, but on who can pay the highest fees. In effect, vendors buy market share from the GPOs for exclusive access to their member hospitals. The more they pay, the more market share they receive. As a result, many vendors favored by GPOs enjoy monopoly status.

Today, corruption in these markets is so extreme that hospital executives themselves are often offered a cut of the fees from GPOs. In 2013, one analyst said that “many hospital executives who are part of the Premier alliance have learned to rely on that share back as an integral part of their annual compensation.” In other words, hospitals are buying supplies at inflated prices, and those suppliers use some of that extra money in direct bribes to hospital executives.

| Video gifs by quotes | fb984966 | 紗")

The legalization of kickbacks happened as a series of mergers in the 1990s consolidated power within the industry. In 1995, Premier Health Alliance, American Healthcare Systems, and SunHealth Alliance merged into the nation’s largest GPO, Premier. By 2017, the giants in the industry - Vizient, Premier, HealthTrust, and Intaler - came to manage $300 billion of hospital purchasing for 5000 health systems, or 90% of total medical supplies in the United States. These GPOs have deals with the three major distributors - McKesson, AmerisourceBergen and Cardinal Health - which precludes any smaller distributors from getting into the business. At this point, 90% of generic medicines are bought by just four firms.

And this consolidation and restructuring of hospital buying has ruined the American supply chain, and prevented the ability to rebuild it.

Why Can’t We Make Masks?

In 2003, according to mask production executive Mike Bowen, America made 90% of its own masks and respirators. By 2005, America imported 90% of its masks and respirators. In just two short years, the entire supply chain moved abroad. Why did this happen? Bowen laid the blame at the feet of GPOs.

GPOs were blocking new entrants, like makers of innovative devices like retractible syringes and infant-ready pulse oximeters, because the firms couldn’t pay their administrative fees. (Several firms, like that which made retractible syringes, eventually won an antitrust suit against two GPOs, syringe monopolist BD, and Tyco.) What was happening is that Bowen, a domestic producer of masks, simply couldn’t get a contract with GPOs. GPOs require a national sales force, including clinicians to get into the sales channel, as opposed to how it used to work, which was selling hospital by hospital. Only large national firms can compete with such requirements.

Like Amazon does to small vendors and third party sellers, GPOs pressure small producers to give them higher and higher administrative fees, ultimately destroying their margins and causing them to either offshore production or use substandard factories that would force a recall or factory shutdown. (Indeed, one reason for the shortage of tubes used for critical blood clot testing is a recall by one of the major producers last year.) GPOs also inflates cost: when a small competitor was finally allowed to compete with Tyco (now Covidian) over oximeters, prices dropped by 30%. Some experts put GPO-hospital-supplier cartel cost at $100 billion annually.

Along with higher cost and less innovation, there is also the pooling of production and risk. As Phillip L. Zweig and Frederick C. Blum noted in 2018, one reason the U.S. has been importing saline solution - aka salt water - for years is because GPOs rely “almost exclusively on Baxter for these products.” And Baxter not only didn’t produce enough, causing shortages and thus reliance on imports, but also put its key plants in Puerto Rico, which was devastated by Hurricane Maria. The pooling of production led to pooling of risk.

In other words, the reason supply and demand isn’t working in medical markets for devices, supplies and medicines is because the system is a giant cartel of hospitals, suppliers, and distributors, glued together with Group Purchasing Organizations who serve as the middlemen. They have set up a brittle and fragile system which doesn’t respond to price or quality signals, and creates incentives for shortages.

Moving Forward

Of course, GPOs and hospitals couldn’t do what they do without political power. So what happened with the Senate investigations? Ultimately, they petered out, blocked by powerful Senators like Chuck Schumer and regulators who never saw a kickback they couldn’t get behind. These middlemen have bought up everyone in the industry. Here, for instance, is a comment to the FTC on the wonders of GPOs, funded by the industry and authored by among others former Obama FTC Chairman Jon Leibowitz.

More to the point, hospitals are political giants, intimidating politicians and generally using their medical authority as cover for these kinds of schemes. (You’ll notice, for instance, that left-wing politicians often go after pharmaceutical firms for high prices, but rarely use that rhetoric against hospitals.)

That said, people who work in the medical supply industry understand exactly what is happening. And increasingly, so does the political establishment. The Food and Drug Administration noted the problem in 2019. And in the White House’s 100 day supply chain review, Biden’s supply chain task force mentioned GPOs and sole source contracts repeatedly.

So we know the problem. What we need is Department of Health and Human Services to do oversight on GPO kickbacks and narrow them, and for Congress to just reimpose the anti-kickback rule. (This bill would probably do it) The shortages won’t go away instantly. But at least firms in the medical supply chain would stop competing over who can get more kickbacks, and start competing over who can best make and sell stuff that patients and doctors need. And all the other investments the government is making in production would start to bear a lot more fruit.

The reason doctors and medical personnel are complaining about shortages is because the administrators of hospitals are in a buying cartel that produces them.

How the Federal Reserve Caused a Massive Merger Wave: In March of 2020, Congress and the Federal Reserve coordinated in joint actions to backstop the financial markets, which were going haywire because of the pandemic. This was encapsulated in the CARES Act, which legitimized the endless bailouts from the Fed towards private equity and the corporate sector.

At the time, I called it a ‘corporate coup,’ explaining through what is known as the Cantillon Effect that money printing as it was done would lead to significant corporate consolidation. And so it has. The Wall Street Journal reported that after only 8 months, 2021 is the biggest year for M&A since they started keeping records. One McKinsey consultant recently put it, “When you’ve got the Fed saying debt will stay cheap for years, plus historically high multiples, the numbers look buoyant — especially if you’re a seller.”

This was all predictable. In April of 2020, my organization plus a number of nonprofits warned about the problem, sending a letter to Fed Chair Jay Powell asking the central bank to put restrictions on monetary actions to stem massive consolidations. Multiple members of Congress, led by Elizabeth Warren, tried to put a temporary merger prohibition into the various pieces of legislation then wending their way through Congress.

Powell, unfortunately, ignored the warnings he was receiving, and Congress didn’t enact a merger prohibition. Noah Phillips, the Republican FTC Commissioner who opposed Trump’s antitrust suit against Facebook, attacked the idea of a merger ban, saying that the FTC was not overwhelmed with merger filings. “There is no evidence of a merger “wave”, or that the [FTC] is overwhelmed with HSR filings,” he wrote on a well-known libertarian blog. Of course, the signs of a coming wave were obvious, but Phillips didn’t want to see them.

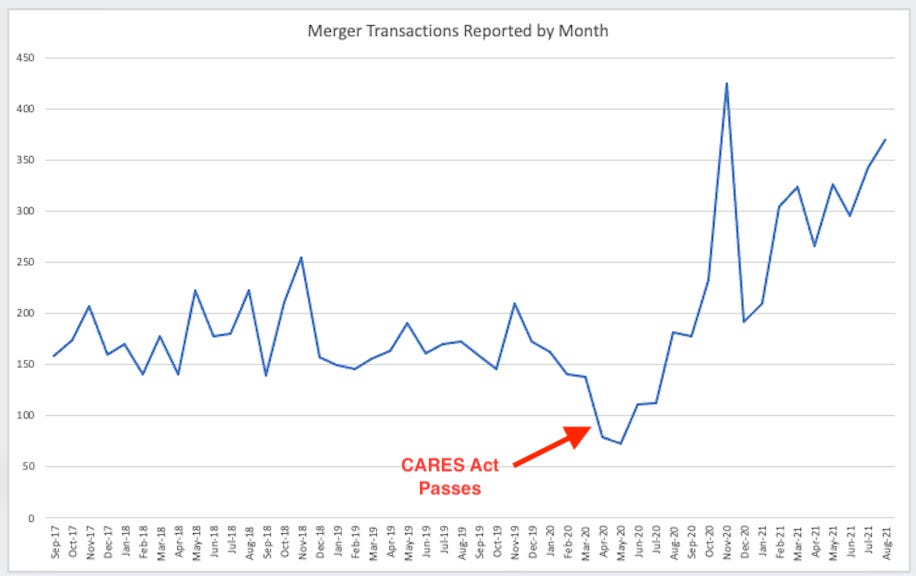

Flush with cheap government backstopped capital and little resistance from antitrust enforcers, Wall Street went crazy with mergers. Here’s a chart I put together using Hart-Scott-Rodino data from the Federal Trade Commission, a law that requires firms to report mergers over a certain size.

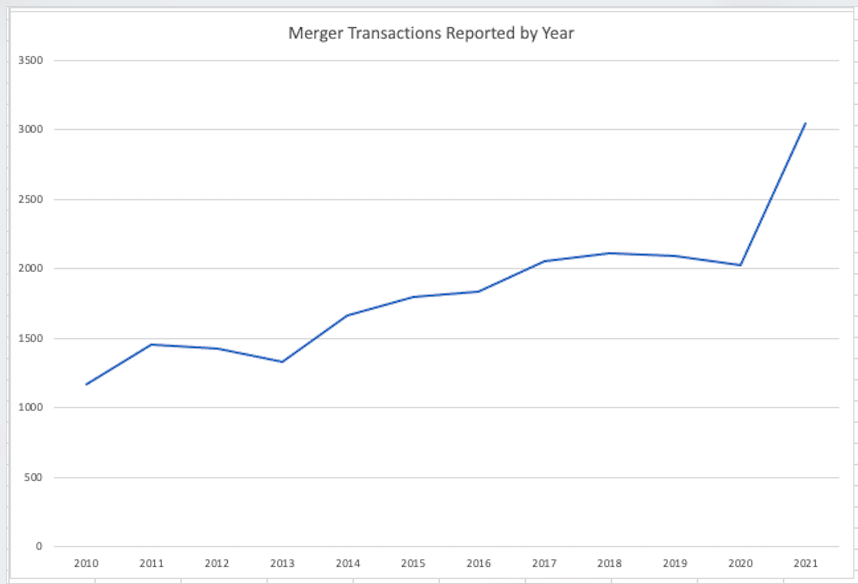

Already the number of mergers in the first eight months of this year has far surpassed the total number for all of last year. Here’s an annual chart, with a projection of the total number of mergers for 2021 based on the current pace of transactions reported.

And this gets to the administrative problem at the agencies. Antitrust officials have 30 days to evaluate whether a merger should be investigated, and then they can ask follow-up questions. If they still want to investigate, they get a few more months to challenge the merger, which means putting together large, complex commercial litigation in a very short amount of time. If they don’t, the firms will go ahead and combine operations.

As the burden to prove a merger is problematic increases due to monopoly friendly judges, the workload has gone up over time to stop any particular merger. It’s not impossible to stop them. In July, the Department of Justice stopped insurance giants Aon PLC and Willis Towers Watson from combining. But each one takes a staff going through millions of documents, even when the merger is obviously illegal. And as the number of filings goes up, and the agencies begin going after big tech through suits against Google and Facebook, the workload becomes crushing. To put it differently, the workload of the agencies has gone up by 50% since the CARES Act passed and Jay Powell subsidized a merger wave.

A simple fix would be to tweak the merger process and let U.S. enforcers operate like European agencies, which is to say allow them to stop firms from combining operations until they are cleared to do so. There are many other possible fixes, like legislating rules that block mergers above a certain size, or stopping mergers when there are fewer than five firms in a market. But right now, the antitrust enforcers aren’t just trying to stop mergers, they are also fighting the Fed’s cheap money policies and lax regulatory choices encouraging such combinations. Congress should pay some attention.

Lina Khan Lays Out Priorities for an Overwhelmed FTC: Last week, new Federal Trade Commission Chair Lina Khan laid out her priorities for the FTC in a widely circulated memo. It’s a very important document, because expectations for Khan are very high, and how she prioritizes will go a long way towards indicating whether her tenure will be successful.

In this memo, Khan indicates her goal of pulling the FTC from its traditional role of going after one-off violations and rip-offs, and striking at root causes and big firms. That means thinking about market structure itself, not just harm to consumers, as well as moving beyond economists and bringing in different sets of experts. She also indicated a desire to further democratize the agency, which means more open meetings, and potentially open more regional offices outside of D.C. to reflect the nation as a whole. Already they have opened comment periods to hear about unfair contract terms, with several thousand having been received already.

In terms of policy priorities, the FTC will focus on consolidation in general as a problem, dealing with the overwhelming merger wave and trying to find ways of deterring obviously illegal transactions so they don’t suck up resources. New merger guidelines will be a key part of the anti-consolidation push. Khan also wants to focus on “dominant intermediaries and extractive business models,” aka middlemen who use “their critical market position to hike fees, dictate terms, and protect and extend their market power.” Private equity gets a mention as stripping productive capacity and distorting business incentives (which is a huge change since antitrust enforcers tend to like private equity, seeing it as a force that introduces more competition.)

And finally, she wants to explore unfair contract terms, take-it-or-leave type of stuff. She wants to go after “non-competes, repair restrictions, and exclusionary clauses,” based on the comments the FTC is hearing from the public. Khan has a hard job for a lot of reasons, not the least of which is that the merger wave the Fed and Congress engineered is inundating the FTC.

“Accountability is coming:" Did Mark Zuckerberg Violate Insider Trading Laws? It’s been a bad few weeks for Facebook.

First, the media has shown a lot of the firm’s very dirty laundry. The Wall Street Journal reported last week that the social media giant had internal research showing that Instagram makes teenage girls want to kill themselves. This follows a story showing that the firm has a special elite set of users exempt from normal rules, as well as one showing how the firm encourages angry behavior to sell more ads. Then the New York Times has revealed that Zuckerberg taken to tweaking the algorithm of its news feed used by 2 billion people to show users positive stories about his own image and that of his firm.

In Congress, Facebook didn’t fare much better. “Accountability is coming.” That’s what Senator Josh Hawley told Facebook lobbyist Steve Satterfield after Satterfield lied, dissembled, and did everything but take a crap in front of the Senate Antitrust Subcommittee yesterday.

I’m only exaggerating slightly. It’s evident the firm has decided to stonewall and go on the attack; Zuckerberg is done with insincere apologies, and done modifying business practices to get better PR. He believes that he will be pilloried no matter what, and that no one will stop him from doing what he wants to do anyway.

The results of this strategy weren’t pretty. Senator Richard Blumenthal quoted Hawley at the hearing, and both Democrat Amy Klobuchar and Republican Mike Lee let Satterfield have it as well, getting visibly angry at his stonewalling. “That’s not an answer to my question,” Klobuchar told the Facebook lobbyist at one point. And Klobuchar is not just nice in public, but Minnesota nice. She tries to avoid overt conflict. This time, she didn’t. She was mad.

But the worst thing to befall senior leaders and ex-leaders at Facebook was, as Jason Kint noted on Twitter, this lawsuit filed in Rhode Island by a bunch of union pension funds.

The plaintiffs accuse a whole host of insiders at the firm of malfeasance, not just Zuckerberg and Sandberg, but Netflix CEO Reed Hastings and Biden Covid czar and former Facebook board member Jeff Zients.

It’s a very long complaint, but the gist is pretty simple. The first part is that Zuckerberg knew he was violating the law, and in particular the Federal Trade Commission order barring Facebook from deceiving users. And he did it anyway, with the tacit acquiescence of board members like Zients and auditing firms like PwC, which assessed the firm’s compliance with the various FTC consent decrees. The second part, and this is where it gets interesting, is that when he realized his lawbreaking would be exposed via reporting on Cambridge Analytica, he sold huge blocs of stock.

And the timing is very suspicious. While Zuckerberg had pledged to only sell $1 billion of stock a year in 2015, after he “learned of Cambridge Analytica’s massive extraction of Facebook user data, he and the entities controlled by him significantly accelerated his sales of Facebook shares,” selling roughly $10 billion of stock while he had material non-public information about the firm. Sandberg did the same thing, as did WhatsApp founder Jan Koum, and a host of others. (One irony here is that this was a losing trade, because Facebook’s stock is higher today than it was then, and no doubt this will be part of their defense. It’s also an irrelevant fact, since trading on non-public information is the offense.)

There’s a lot more in the complaint, but I’m focused on this particular nugget because insider trading is a criminal offense. Crime shouldn’t pay, but it’s clear that Zuckerberg simply does not believe anything will happen to him until something does. And while there is a crisis of credibility in our government, the two regulators that I would not want to mess with are FTC Chair Lina Khan and SEC Chair Gary Gensler. Zuckerberg might have put himself in the cross-hairs of both of them.

There are many reasons that Mark Zuckerberg and Sheryl Sandberg might be indictable for criminal activities. Throw this one on the pile.

Thanks for reading. Send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

Philip Zweig has been (is) such a fierce outspoken advocate against these kickbacks but faces a David vs. Goliath situation in a purposefully obscured area of healthcare policy and decision-making. It is more than shortages and the harm from not having the right product at the right time. The game-playing and anti-competitive behavior makes hospitals less safe - the best (whatever criteria - mix of price and quality - a consumer of healthcare goods would use to judge "best") products don't win out. Adam Smith himself understood the danger of monopolies, right?

The game-playing in the hospital supply chain can result in products being switched out for no reason other than a backroom deal; that change increases risk as staff need to adjust. I worked in hospitals in patient safety and risk; this happens.

I think we need much more transparency into the books of all companies that work in healthcare - profit or non-profit - to see what is hidden. I don't see that happening so long as our economy is captured by big business or - in healthcare - what is sometimes called the medical-industrial complex (which, in my view, includes the AMA).

I also don't think most hospital staff know leadership has a financial stake in decisions made to choose/reject products and supplies. It is bizarre but it is almost like hospitals need internal air-tight bans on voting/weighing in on decisions where one has a financial conflict-of-interest (disclosure being wholly inadequate) - including at the Board level.

Indicting Zuckerberg, then trying, convicting, and sentencing him to time in prison would go a long way toward restoring the faith of the American people in the American justice system. Doing the same to the former guy would go even further.