How a Cheerleading Monopolist Played Rough During the Pandemic

How a Cheerleading Monopolist Played Rough During the Pandemic

After mass layoffs, Bain Capital's Varsity Brands is now a "cash flow" machine. It also faces risks from an increasingly angry cheer community.

Hi,

Welcome to BIG, a newsletter about the politics of monopoly. If you’d like to sign up, you can do so here. Or just read on…

Today I’m writing about how Varsity Brands, the cheerleading monopolist, has handled the pandemic. Like many monopolists, at first it looked like it was in trouble, then it was hit with legal problems, and now it’s doing better than ever, raising money and appearing to issue threats to competitors. Plus:

AT&T concedes its merger with Time Warner failed.

In a major power move, Republicans on the Senate Commerce Committee overwhelmingly supported progressive trust-buster Lina Khan.

Why Are There Shortages of Plastic Bags Needed for Vaccine Production?

Also, I was on Rising with Saagar Enjeti and Krystal Ball to talk about the Biden administration’s attack on vaccine monopolists.

And now….

Varsity Brands’s Valuable Monopoly

Last January, just before the pandemic, I wrote up one of the more interesting monopolies I’ve seen, which is a Bain Capital-owned firm named Varsity Brands that has rolled up power in cheerleading. Yes, cheerleading, the gymnastics-style team sport, largely but not entirely female, where young athletes don sparkly uniforms and do incredibly dangerous and difficult stunts.

Cheerleading is a tight knit community, and the people in it - parents, coaches, cheerleaders, judges, event producers, gym owners - care deeply about ‘the spirit of cheer.’ The sport is important to millions of young people, who make lifelong friendships and gain confidence and pride in themselves. And yet, it’s also incredibly expensive for no good reason. Parents tell me they are shocked at the prices for equipment and events; some take second jobs to afford the high fees, because that’s how much their kids love it.

In this close-knit passion for a common activity, cheerleading is not so different from most industries. In Silicon Valley in the 1970s, for instance, there was a bar called the Wagon Wheel where semiconductor engineers would meet and exchange gossip excitedly about the latest discoveries. “Information travels at the speed of beer,” was the expression. People are often passionate about what they do, no matter how nerdy or weird, and industries are social networks and identities as much as they are mechanisms to produce goods and services. Go on to the dating site FarmersOnly if you don’t believe me.

And that’s why I love the saga of Varsity Brands. There’s a real human story, a community of people that love a youth sport and the act of growing up, intersecting with the worst trends in American business. After all, if there’s a monopoly in something as idiosyncratic as cheerleading, then it’s evident corporate concentration is a systemic feature of the American economy, where monopolies aren’t just massively powerful institutions like Google and Comcast, but are firms like Varsity in niche markets too. As Harvard antitrust professor Einer Elhauge noted, a cheerleading monopoly shows that most of the economic theories policymakers have been using to see corporate power are wrong.

Cheerleading became a monopoly the same way that most monopolies form in America, through mergers. Over the course of a few decades, Varsity bought up 80-90% of the cheer contests, the most significant one being its purchase of Jam Brands in 2015. It also gained control over the nonprofit rule-making organizations for the sport, most importantly the U.S. All Star Federation, which it financed and staffed.

With control over the rules of the sport, and how the tournaments worked, Varsity gained power over the gyms where athletes train. It raised prices for its events, and charged inflated amounts for apparel, uniforms and equipment. At the same time, it gave secret rebates to gyms based on how many tournaments they attended and how much apparel they bought. Gyms and independent event promoters operated in fear of Varsity, not just because of this rebate system, but because Varsity determines which teams got to go to the best tournaments, and even the scoring systems deciding who wins and loses. Its control over the sport, and resulting pricing power over apparel and equipment, was so iron-clad that CNBC called Varsity one of the “few retail businesses of scale that may also have an Amazon defense.”

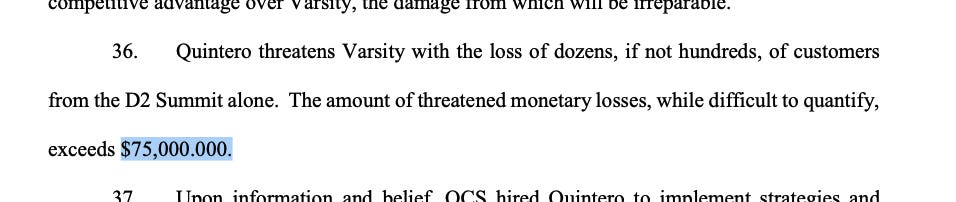

In a March filing of a lawsuit against a former employee, Varsity’s legal counsel, William S. Rutchow, told the district court that if it were to face significant competition for just one tournament, the D2 Summit, its losses could exceed $75,000.

[UPDATE: This section of the piece has been updated with a correction. I originally wrote that it was $75 million, as it is drafted as $75,000.000 and the rumors I was told were that such tournaments generate in the tens of millions of dollars of profit, so it didn’t seem outlandish. That said, a few readers noted that this number is probably a typo. In reviewing it again, I think it is a typo. I asked Rutchow, and he kindly got back to me with a correction that the intended number is $75,000. Apologies for missing this one!]

Varsity’s During Covid: “A Cash Flow Machine”

Two months after I wrote about this cheer monopoly, Covid hit, and nearly all live events and sports businesses, including cheerleading, shut down. Varsity reduced its workforce by thousands, cut employee pay, and canceled contests. But problems for Varsity extended far beyond the virus. In May, a law firm filed the first class action antitrust suit against the cheerleading giant, with several more filed since. Even worse, in September, USA Today uncovered a scandal of sexual predators in the sport, linked to the USASF, the nonprofit governing body controlled by Varsity.

One would generally think all of these problems, and a pandemic shutting down most live events, would be bad for Varsity’s business. But in fact, Varsity seems to be doing better than ever. In the midst of the pandemic, CEO Adam Blumenfeld announced they had raised $185 million in just ten days, four times what they originally sought. “This amount is distinguishable and differentiating in our marketplace,” he said.

And as it turns out, the pandemic was in other ways very good for Varsity, beyond just getting cheap capital. Bain Capital had been trying to clean house after buying the firm a few years ago, and it was able to do so with its layoffs. And canceling live events wasn’t necessarily bad for the corporation, because it had monopolized the space. As one industry participant told me, Varsity was able to get teams to compete virtually, and had virtually no costs - no stages, setup, or event costs beyond web streaming. “Varsity is a cash flow machine,” one person in the industry told me. Their costs dropped by 80-90%, but their fees only declined by a third. It’s no wonder that, according to the Dallas Morning News, Varsity has “grown its cash pile during the pandemic.”

Antitrust Suits Drive Competition

It’s not all good news for Varsity. One of the consequences of the increased scrutiny caused by the antitrust suits is an explosion of anger within the tight-knit cheer community. Some gym owners, apparel makers, parents and event producers decided to get out from under Varsity’s shadow, and shift, as one person told me, “towards a free and ethical market.” With the lawsuits pending, people in the industry became slightly less afraid. And they started competing.

As Varsity reduced the number and quality of its events (mostly the smaller, less profitable regional events were the ones to go), independent event producers, roughly 10-15% of the industry, began to innovate to fill in the gaps, subtly challenging Varsity’s power. Event planners started filming and streaming teams at their own gyms, and setting up new forms of virtual contests outside the control of Varsity. eCheer.TV launched, challenging VarsityTV.

A few event producers even went after the source of Varsity’s dominance by creating their own cheerleading championship, called the All-Star Worlds. This rival championship tournament is a mortal threat to the cheerleading monopolist. Varsity’s power over gyms, event producers, coaches, judges, and the whole industry comes from its ability to pick and choose who gets to go to its prestigious championship tournaments. So the prospect of a championship they don’t control threatens their entire apparatus, and their ability to inflate prices across the board. If there are multiple championship tournaments, Varsity can no longer write rules for the sport or use threats to choose which teams get to succeed, or which event producers succeed. As Varsity’s lawyer noted, its pricing power becomes a lot less potent.

So when someone finally organized a rival to one of Varsity’s championship tournaments, the USASF sent a letter to every event producer that chose to participate, saying it would kick them out of the cheerleading world if they participated in the new tournament. Varsity also used other tactics; it sued a former employee who went to work for its rival. (There are also rumors of pressure they put on gym owners who attend the rival championship tournament, but I couldn’t verify them.)

This kind of behavior seems aggressive, especially since Varsity is under threat of antitrust suits. But as one contact told me, “Antitrust suits are not slowing them down at all.” And why would Bain Capital do anything but encourage the most aggressive behavior possible, considering that every other monopolist seems to go scot free? “They don’t think they are going to get into trouble,” I was told, “as nobody else is getting in trouble.”

It’s not entirely clear what happens after the pandemic, whether Varsity rehires its staff and begins planning smaller and regional events again, or if it tries to retain a hybrid of virtual and live events, with its lower cost structure. But taking a step back, the larger story here isn’t just about cheerleading, but about what our monopoly-friendly policy framework is doing to our society, our businesses, and our kids. Bain Capital’s goal is to generate as much cash as possible for as little cost as it can, and it will extract what it can however it can, and its subsidiary firms will threaten who they must to keep the game going.

More broadly, the American economy today is divided between normal firms that have to make it by selling goods and services, and private equity-connected firms like Varsity that have access to unlimited capital and don’t seem to encounter the rule of law. Varsity’s opponents can put on contests and do a good job, but they must do so under legal and economic threat, and without the absurd capital cushion of their monopolist rival.

Ultimately, for Varsity, it’s a rational choice to engage in predatory behavior when there’s very little chance the government will enforce the antitrust laws. There’s a lot of noise these days about antitrust, and the Biden administration will hopefully pick someone to run the antitrust agencies who will likely be more aggressive. So I think what Varsity is doing is a mistake, as well as a moral wrong. But while what Varsity is doing may be a bad bet, it’s a bet every other powerful corporation is making, and a bet they will keep making until somebody stops them.

The AT&T-Time Warner Merger Failed: Three years after its $88 billion merger with Time Warner, AT&T is now trying to spin off its media assets and combine them with yet another media conglomerate, Discovery. There will be a lot to say about this attempt to further consolidate the media business, but it’s important to underscore a basic point. The AT&T-Time Warner merger, like most mega-mergers, was a disaster, causing layoffs, acrimony among artists, and eroding the HBO brand, which was one of the highest quality brands in Hollywood.

There was never any logic to this stupid merger except that Jeff Bewkes, Time Warner’s then-CEO, wanted his $400 million golden parachute. There are times when mergers can be useful, such as if there’s a failing firm, or a business owner wants to retire or try something new. But these mega-mergers are ridiculous. As we rethink merger law, it’s time to recognize that mergers are usually destructive, and corporate leaders should have to prove that a corporate combination is a good idea before the government lets it go forward. That’s how much of 19th century political economy worked, and it made sense. The AT&T-Time Warner fiasco, on top of dozens of other fiascos, is a good example of why.

(A key purpose of the new WarnerMedia and Discovery merger is layoffs and reduced power by creators, which is why AT&T is bragging about $3 billion in ‘synergies.’)

Antitrust Establishment Confused as Big Tech Foe Lina Khan Gets Overwhelming Support from Congress: One of the more remarkable appointments Joe Biden has made is that of Lina Khan to the Federal Trade Commission, which is one of two government departments tasked with enforcing antitrust laws. Khan made her bones exposing how lax antitrust law enabled Amazon’s dominance, so when he nominated her, the antitrust establishment was utterly horrified. “Putting more extremists on the commission is not the way to do better,” said University of Pennsylvania law professor Herb Hovenkamp.

Hovenkamp, who is generally a booster of large technology firms, told the National Journal that Khan’s “radical views” make it hard to see how she could get any Republican votes, and she might even fail to be confirmed. Hovenkamp is not some random expert, he has been cited by the Supreme Court in 38 different cases. It’s not just Hovenkamp. Fiona Scott Morton, a Yale Business School professor (adjunct at the Law school) who started a center at her university to study monopolies after working in the Obama administration’s often criticized antitrust division, also had choice words about Khan. “Having radical ideas is fun, but it’s not what the day job is going to be.” Morton’s public lobbying against Khan is likely ideological, not a result of her consulting contracts with Amazon and Apple. But it is still shocking.

Last week, Khan not only got every Democrat in the Senate Commerce Committee, but eight out of twelve Republican votes. That means she’ll probably get something on the order of 70-80 votes on the floor of the Senate. It’s a signal that Congress wants action on big tech, and they prefer progressive trust-busters to meek technocrats. What once was fringe is now mainstream, and vice versa.

Why Are There Shortages of Plastic Bags Needed for Vaccine Production? One of the main arguments from the pharmaceutical industry against waiving certain intellectual property rights in the pandemic is that supply chain shortages, not patents, are the limiting factor in vaccine production. In a piece titled “Patents are Not the Problem!”, for instance, libertarian economist Alex Tabarrok popularized the line “Plastic bags are a bigger bottleneck than patents.”

And yet, these libertarians and pharmaceutical industry defenders don’t attempt to explain why such shortages are pervasive. Vaccine manufacturing supplies, including single use bioreactor bags, are not only in short supply because of exceptionally high pandemic demand, but also because there’s been a classic monopoly rollup of the bioprocess supplies industry in recent years. That consolidation is fortified by extensive intellectual property barriers that prevent new entrants from manufacturing these now crucial bioreactor bags and filters, including 2,800 patents granted on single-use bioreactor bags over the last couple of decades.

There are four dominant players in this market: Merck, Danaher, Sartorius, and Thermo Fisher. The current industry structure is a result of a systemic roll-up in the industry, largely so conglomerates could have a full integrated suite of products to offer to pharmaceutical buyers, as well as the pricing power in doing so, in addition to extensive intellectual property thickets. Merck acquired Millipore in 2010 and Sigma-Aldrich in 2015, Thermo Fisher merged with Life Technologies Corporation in 2013, Danaher bought the Pall Corporation in 2015 and GE’s giant Healthcare biopharma business, and so forth.

Now we have a concentrated and excessively bureaucratic industry, in the midst of a pandemic with massive demand. The government needs to go on an emergency trust-busting spree using every tool in its arsenal. Waiver and compulsory licensing of monopoly patents throughout the supply chain could potentially address bottlenecks, which is why India and South Africa included the entire supply chain as part of their waiver proposal to the WTO.

More than that, the government needs to begin the process of unwinding these mergers, and forcing standardization of equipment. Finally, public agencies should aggressively finance new entrants. So yes, we need to waive IP for vaccine production. We also need to do a lot more, and we don’t have time to waste.

Thanks for reading. Send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

P.S. I’m on vacation, so I won’t be sending out a newsletter next week.

Matt, I haven't finished the article yet, but I had to take a break to thank you for the clarity of your writing. I'm old and old-fashioned, I guess, but I grew up in a time when clear writing was expected. At one modern day point, I was beginning to wonder if there was something wrong with me. It seemed that writers were beginning - not at the beginning - but in the middle. It's as if one walked into a party late and joined an ongoing conversation where everyone knew the who, what, and why but the newcomer.

I began to feel as if the writer were crafting a mystery and I had to pit my wits against the author to figure the thing out.

So just a brief interlude to say that the clarity of your writing is a joy to read. Now I go back to the article. And then I have to check out the Farmers Only site. :-)

Thanks for the good news, Matt.