Can We Even Stop Monopolization in a Pandemic?

Can We Even Stop Monopolization in a Pandemic?

These four examples show that it's hard to tell the difference between consolidation and healthy adjustment to a pandemic.

Hi,

Welcome to BIG, a newsletter about the politics of monopoly. If you’d like to sign up, you can do so here. Or just read on…

Today I’m going to list four examples of how the pandemic is enabling consolidation, and then observe why control of corporate assets fundamentally is a question of whether we live in a democratic society or an authoritarian one.

Competing Narratives Around Monopolization

Today I was on a phone call with a German journalist about monopoly power, and he asked me a set of questions I receive fairly frequently. Isn’t a monopoly, he asked, just evidence that a corporation had a better product than the competition? How can you say that monopoly power is a result of anti-competitive tactics?

The answer to these questions is complex. Many monopolies (though not all) start out with an innovative product, and then morph into political protection rackets to protect what was once a compelling product but is now purely a cash cow. Google for instance launched a great search engine, garnering it market share in search in the early 2000s. In 2002, the corporation began a merger strategy, and within just a few years it had a sophisticated political operation designed to ward off privacy laws and antitrust suits. Mark Zuckerberg’s Facebook product was pretty good in 2004, but there’s little innovation coming from Facebook these days. He has however restructured his board of directors to build political protection in a Republican administration. Similarly, Boeing once made great planes, now it has great connections and big bailouts, an engineering powerhouse turned into a financial engineering powerhouse.

But there’s something important about the question. It is hard to tell the difference between a rapidly growing business and a roll-up of market power. In a pandemic these distinctions can become even more difficult to discern, since there really is a deep need for rapid deployment of capital, often in distressed situations. It is also not always evident whether the attempt to grow is driven by the need for more productive capacity, or by the desire to engage in financial engineering or acquire market power.

And sometimes even the question itself becomes irrelevant, as we simply have no choice but to depend on a monopoly in a crisis, and regulate or hope that the essential service operates in the public interest. You go into a pandemic with the institutions you have, and many of our public institutions are at this point quite degraded, so the only way to operate is through channels controlled by concentrated power. In other words, monopolization and consolidation can happen for what seem to be good, or least necessary, reasons. How we respond as a society depends on how we imagine these concentrations of power came to be. So here are four examples of the growth of market power in this pandemic, some that are more grey area-ish than others, and then a conclusion about what they mean.

(1) Amazon: “No Other Choice”

Amazon’s increasing market power is not surprising. For at least a decade, the online giant has had market power over those trying to retail their products online. But with most retail stores shut down, Amazon has been extending its power over all retail, forcing brands who could stay off the platform onto its terrain. Amazon’s sales were up 24% in the first quarter, in a terrain where consumer sales are declining. If you had offline channels through which you could sell before the pandemic, now you really don’t.

Supplicants to Amazon make the point. Here’s Josh Cowan, a former Amazon executive who now helps brands sell through the company, talking to Bloomberg: “Brands are absolutely terrified to be reliant on Amazon right now, but they have no other choice.” That’s market power.

Here’s Ivory Ella CEO Cathy Quain, who sells “save the elephants” t-shirts and hoodies and donates proceeds to wildlife conservation, and has traditionally kept off the platform by selling to offline retail stores. “It’s a necessity for us to be where people can shop,” she says. That’s market power.

It’s not just in the retail space that Amazon is wielding its power, the corporation also radically cut the fees it pays to affiliates and publishers for getting customers to visit Amazon and buy products. An entire ecosystem, which is from what I’m told fairly leveraged up, will now collapse, simply because Amazon is the only game in town for customers and doesn’t need to keep paying for marketing.

And what of antitrust enforcers? As Bloomberg observes, “Bezos, who has compared his warehouse workers and delivery contractors to Covid-19 first responders, is betting that strengthening Amazon’s position won’t provoke antitrust regulators already investigating the company.”

So that’s the essential facility excuse.

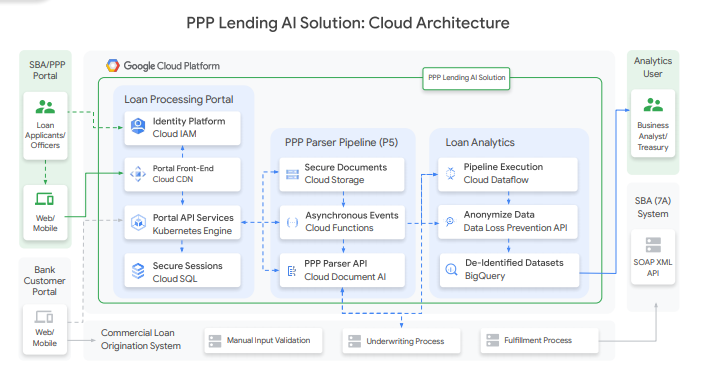

(2) Google Moves Into Bailout Banking

This one’s a bit more speculative, but Google is now attempting to become infrastructure for banks and brokers with its “PPP Lending AI Solution.” Google is offering a product that lets banks and borrowers upload loan documents, and then parses those documents for key data useful in originating loans. This is their marketing spin:

Leveraging artificial intelligence, we’ve created an end-to-end solution that speeds up the time-to-decision on loans and helps inform lenders’ liquidity analysis—from the initial application submission to the underwriting process and SBA validation. The solution is also equipped with Google’s security capabilities, enabling lenders to meet policy requirements and protect critical assets.

The key tell that there’s a power grab here is that “the product will be offered to lending institutions at no cost.” There is no free lunch, so if the price is not upfront, it’s buried somewhere in the back, usually in the form of a tacit handover of market power in one form or another. Google has other financial services products, where it enables banks to “predict credit and loan defaults and margin calls,” and to comply with stress testing and regulatory requirements. Basically, Google is seeking to become the guts of a bank, while letting bankers keep the branding and liability and all that other messy stuff.

In fact, my guess is that Google is attempting to be the guts of every bank. There’s already an oligopoly in banking software (known as ‘core’ software), and I’ve talked to a bunch of bankers who just absolutely despise their core software, which is often expensive, hard to use, and buggy. No doubt Google sees the pandemic as a moment to help capture that market for itself as bankers transition their infrastructure off of much older mainframe technology.

This dynamic is similar in some ways to Google’s penetration of the educational market. Bad educational procurement policy led to a horrible educational technology market. Google, by giving away reasonably high quality product in order to capture student data, was able to capture market share quickly.

Google is probably making the argument that banking software is competitive, and that this offering is an improvement on what is out there, helping banks lend to small businesses and comply with government rules. And the product free, or so they say. What could be wrong with that?

(3) Cheesecake Factory

I love the early termination notices part of the Federal Trade Commission website, because it tells you every day which transactions the Federal Trade Commission cleared. An early termination means the FTC didn’t ask any real questions about an acquisition, and just waived it through.

Last week the FTC cleared private equity fund Roark Capital Partners and its purchase of a stake in the Cheesecake Factory. Roark Capital is a franchise conglomerate, with “investments in franchises/multi-unit brands generate $41 billion across 89000 outlets.” These investments include Jamba Juice, Arby’s, Sonic, Rusty Taco, Jimmy John’s, Buffalo Wild Wings, Seattle’s Best, McAlister’s Deli, Moe’s Southwest Grill, Schlotzsky’s, Cinnabon, Auntie Anne’s, Miller’s Ale House, Culver’s, Carl’s Jr. and Corner Bakery.

It’s not clear to me how Roark Capital operates, they make the usual noises about long-term growth, etc, and they hold their investments for a long time. Roark Capital is named after fictional character Howard Roark from libertarian Ayn Rand’s novel The Fountainhead, though the firm maintains that the name “does not signify adherence to any particular political philosophy,” merely admiration for the “qualities embodied by Howard Roark.” Ok. Certainly the fund is a specialist in franchising, if not quality literary reviews.

It wasn’t necessarily a bad decision to clear this investment. It is very possibly a reasonable investment from someone with capital to a quality company in need. I can also imagine different ways that Roark Capital exploits market power across its portfolio. What struck me about this deal is that a fund that collects restaurant brands and owns tens of thousands of outlets got clearance to acquire more, without any questions from the FTC. I just see no reason to let this purchase go through without asking any questions. That’s a way to let market power increase without even noticing.

(4) Tele-psychiatry

And finally, this is the most speculative acquisition. Private equity giant TPG recently bought a big stake in Lifestance, one of the largest outpatient behavioral healthcare corporations in the country, basically a collection of psychiatrists and health care workers who address mental health problems.

The corporation seems to be executing on the trend of buying up doctor’s practices, with an acquisition strategy from the get-go when it was established by a few private equity funds. In 2015, the founder of the company said, “These are ‘gold rush’ days in the behavioral healthcare space, and as is typical with a gold rush, it comes with good things and bad things. But there is a lot of money being put to work.” Originally the focus was addiction recovery, but that seems to have fallen by the wayside as Lifestance now addresses other mental health problems.

As you might expect, tele-psychiatry is exploding in the pandemic, as the need explods and as Federal officials relax the rules for tele-health reimbursements. Lifestance is shifting to that work, and TPG is putting $1.2 billion into the company, which is going on a furious hiring spree. There will be more acquisitions in telehealth.

The FTC cleared this purchase quickly, and asked no questions. It could be a useful purchase, or it could simply be degrading the quality of necessary mental health services. Who knows? The FTC sure doesn’t!

Two Narratives

There are two different narratives at work here, one that supports consolidation of corporate assets under the control of a few and the other that is for public control of our social assets through regulated competition.

Here’s the pro-concentration narrative. Amazon and Google, large powerful capable organizations are delivering services we need. Amazon is helping facilitate commerce, and Google is entering a bank software space and helping to move small business lending. Meanwhile, Roark Capital Partners is lending to Cheesecake Factory which needs the capital to preserve its business, and TPG is helping Lifestance expand a needed psychiatric service. The alternative is to let commerce flounder, let banks flounder, block the expansion of necessary medical services, or liquidate otherwise viable businesses.

The anti-monopoly narrative goes as follows. Amazon has eroded its competition so substantially that it is now an essential service, one upon which producers all depend, and one in which workers routinely get the Coronavirus because the corporation won’t spend the resources to protect them. Google, meanwhile, is exploiting a badly structure bank software market to invade yet another crevice of our economy, cross-subsidizing its entrance into this area with rents from its search monopoly. Roark Capital is exploiting a distressed asset to roll up more power in the franchising industry, potentially opening the door to concentrated buying leverage against common suppliers. TPG is similarly aiding in the growth of a large and untested psychiatric service delivery corporation, which could jeopardize vitally important mental health care.

The right approach, in this narrative, is to (a) regulate Amazon in the crisis using public utility rules and labor laws, and then break it up afterwards so we never have to be so dependent again (b) block Google from leveraging its monopoly to enter new markets, and restructure the bank software market to facilitate competition (c) restrict the private equity business model while creating a national investment authority to ensure corporations like the Cheesecake Factory can survive without turning to private equity and (d) make sure that individual practitioners can deliver telemedicine without the need for large roll-ups, or just create a public system to employ medical practitioners if there are genuine economies of scale.

Authoritarian Values versus Democratic Values

As you consider these two narratives, recognize that the differences are not technical, but political. There is no reason that the only funding stream to businesses must come from private equity funds, except that our public policy framework enables the move of our pension money into that particular legal structure, and we have chosen not to build public institutions that can put money to work. Similarly, we don’t have to depend on Amazon, or expect that no one but Google can build usable software, if we choose to regulate our markets to facilitate more competition in niche software markets, or impose public utility rules recognizing the semi-public nature of these enterprises.

These are all simply political choices. We have for decades lacked the will to make our public institutions function with integrity, whether those are bureaucracies that can lend public money in a pinch, or regulators or enforcers who can ensure our corporations compete within ethical bounds. So back to the original question. Is a monopoly the result of a superior product? Not really, no. It’s the result of a lack of confidence in democracy.

Thanks for reading. And if you liked this essay, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you want to a book to hunker down with while sheltering in place, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

P.S. In my last issue I noted the Fed bailed out Carnival Cruise Lines and Boeing. Moody’s issued a report agreeing:

The issuance of US$-denominated IG corporate bonds has received support from special purpose vehicles sponsored by the Federal Reserve. The Fed’s backstop credit facilities may facilitate the recently announced issuance of up to $25 billion of investment-grade bonds by a major aerospace manufacturer for the purpose of assuring sufficient liquidity during a very difficult period for commercial aerospace.

But two readers took issue with my claims. Here’s Michael F:

I used to trade bonds at JPMorgan and Citi. The bonds cleared at an extremely high yield for BBB-paper (Treasury + 4.25%). They are senior secured corporate bonds, which means they're backed by Boeing's assets. Purchasers are likely pension funds and other institutions.

This is not a bailout.

And here’s Alex:

Yes a couple of interesting things here.

The Fed purchasing high-yield (risky, risky) bonds, which most bond investors would otherwise not touch (except Apollo/Elliot with usurious rates & covenants), is absolutely a bailout. The appreciation in market value ($3B according to you) is similar to how legal firms evaluate "damages" to shareholders, so I think this is a roughly accurate assessment of the bailout size. It is money stockholders would otherwise not have but for the Fed intervention.

You argue that the Fed's intervention is "necessary" but "unhealthy"; the alternative is more corporations falling under the ownership of private equity. This part is true. Private equity will either buy these corporations up at firesale prices, or will buy up their debt and foreclose on their assets when they inevitably go bankrupt.

However, I am not sure this is a bad thing. Private equity will own the corporation. If they strip it of its assets and sell them off, it is because it is more profitable to do so. In other words, the corporation probably shouldn't have existed (at least at its size) at that propped-up valuation anyway, else it would be unprofitable to reduce its footprint.

What is the alternative? If not private equity, then these companies stay public. Ordinary people (and their retirement funds) continue to invest in them and impose no financial discipline; ultimately, these investors get bailed out by the Fed.(Keep in mind, if the firms go bankrupt without private equity, the bondholders will foreclose on the assets and sell them off to, or retain them as, private equity anyway.)

If private equity owns them, they'll actually impose financial discipline. If they don't, they lose lots of money (after all, they own these assets and don't want them to depreciate. If you pay $1M for something and it goes bankrupt, you lose, end of story). Private equity has lost a ton of money during this whole crisis. That's how it should be: privatize the losses.All in all, I think Fed intervention is creating a lot of distortions here. It is making capital markets play to what the Fed will do, rather than actually trying to assess the underlying viability of firms. Instead, let firms go bankrupt, let them buy/sell each other, and only bailout those companies which are effectively government utilities (and therefore extremely regulated, such as banks).

P.S. Warren Buffet is essentially private equity, and nobody seems to complain about him! Odd. One may then imagine "private equity, bad" as too reductionist. It is like saying "corporation, bad" or "government, bad". It is too low-resolution.

Psychiatry is not low hanging fruit for PE like ER docs, urology, etc. there is a big undersupply of prescribers in the USA (psychiatrists, nurse practitioners) and health plans have trouble getting enough psychiatrists on their panels. it looks like they are going for critical mass in some states. the best way for PE to make money in psychiatry is restrict prescribers to med management (mainly 15 minute appointments) and to get counselors to provide therapy, which is not always in the best interest of patients. my point being that there aren't a lot of operational efficiencies in psychiatric practice; there are some clinical practice approaches (restrict prescribers to med mgt, use low cost counselors, etc) that could increase revenues. so it looks like TPG is going to be in the business of practicing medicine or at least developing best practices for its employees. Not good.

Good post, Matt. Further to the banking software point, part of the reason the archaic legacy software remains is the time and cost factor associated with migrating to a new solution. And the reason it is such a gargantuan undertaking is mergers and consolidations that have made the big banks almost monopoly like. Smaller banks and credit unions are more nimble and better able to migrate to new systems, while the big guys are left with the old DOS based systems and myriad departmental piecemeal workarounds.