Beef Is Expensive. So Why Are Cattle Ranchers Going Bankrupt?

Beef Is Expensive. So Why Are Cattle Ranchers Going Bankrupt?

Independent cattle producer advocate Bill Bullard explains the problem. It's the monopolies, stupid.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

During the Covid pandemic, Americans went to the supermarket and found something that hadn’t happened for decades - a meat shortage. There was plenty of cattle, but the beef wasn’t getting to the supermarket shelves.

What happened and why?

To answer this question, I asked Bill Bullard, a former cattle rancher and the current CEO of R-CALF, a cattle producer-only membership organization focused on the viability of the U.S. cattle ranching industry. “We have so skeletonized the entire live cattle and beef supply chains that it is no longer capable of withstanding a shock,” he said, “whether it be the covid pandemic or a climatic circumstance.” This shortage was a wake-up call. “The industry is incapable of meeting our national food security needs.”

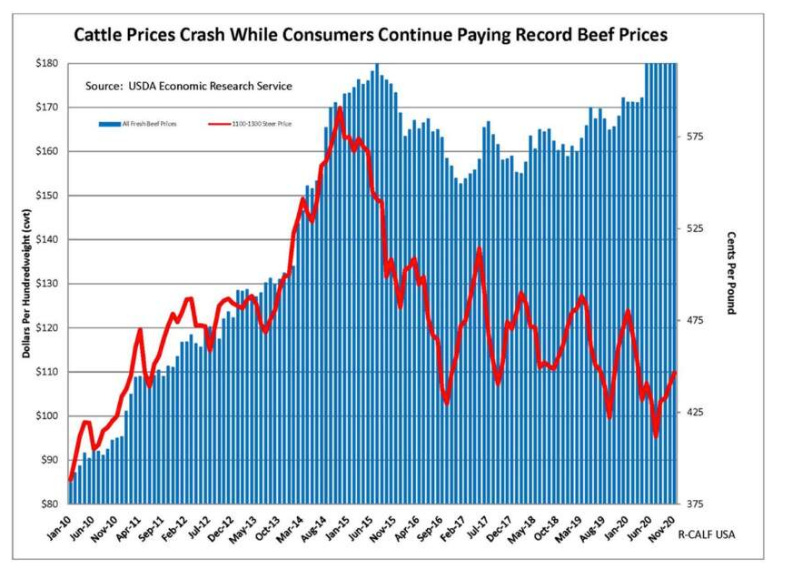

Bullard is an ardent anti-monopolist, a viewpoint developed through hard-won experience dealing with a consolidated meatpacking industry. He noticed problems with our cattle markets becoming more severe in late 2014. That’s when beef prices and cattle prices started to diverge. Such a divergence is very weird, because a lower price paid to farmers for cattle should lead to lower prices for consumers at the supermarket for beef. Cattle and beef prices should move in tandem, like oil and gasoline, since beef is merely processed cattle. And when these price signals do move in tandem, the market works - expensive beef leads to producers selling more cattle, and driving down the price of beef.

Only, what happened since late 2014 is the opposite - even as the beef sold by meatpackers got more expensive, the prices those meatpackers paid to cattle producers went down. Under Covid, this divergence has gotten far more severe, with record prices for consumers, even lower prices for cattle, and at some points, shortages and breakdowns of supply with bare supermarket shelves. Domestic cattle producers are increasingly exiting the industry, even though there’s more demand than ever for their product. Bullard told me that it’s a highly consolidated set of middlemen, the meatpackers, who are grabbing all the profit, charging higher prices to consumers while driving independent cattle producers out of business and ultimately breaking down America’s food system.

In this interview, we went into the nitty gritty of how cattle markets work, or don’t. Enjoy.

Why are consumers paying record beef prices while farmers are getting less for their cattle right now?

The marketplace itself is chronically dysfunctional. You have consumers who have demonstrated a willingness to pay all time record prices for beef. We also have record exports. So this suggests we have incredible beef demand. And yet cattle prices remain depressed. So consumers are paying high prices, cattle producers are receiving low prices, and the middleman is walking away with windfall profits like we've never seen before.

How are our cattle bought and sold these days?

The live cattle supply chain is multi-segmented. The largest segment includes cow calf producers, the farmers or ranchers that maintain mother cows and then have a new calf every year. And the next segment is the yearling operation segment. That's when the calves are grown until they reach the weight where they're ready to begin feeding. And then we have the feeding sector, which is the smallest sector and they feed the cattle to harvest weight, and sell cattle directly to the packer.

How do meatpackers organize their control over ranchers?

Packers have deployed specific cattle procurement methods in order to gain advantage over the marketplace. They have been shifting large volumes of cattle out of the cash market for cattle, which is where competitive price discovery happens, and placed them in unpriced contracts. And we call those cattle captive supplies. That is cattle that are committed to the packer long before harvest, but they're never part of the price discovery process of the industry. And so our cash market is too thin to establish a competitive price for cattle. That gives the meatpackers considerable leverage over the entire supply chain.

How many packers are there?

Well, we have four packers that control 85% of all the fed cattle marketed in the United States. Fed cattle are cattle that are raised specifically for beef production. So we have an unprecedented level of concentration in that sector. There are other regional and small packers, but they only comprise 15% of the available cattle processing in the United States. So the industry is heavily dominated by four multinational meatpackers.

What are those companies’ names?

The companies are Tyson, Cargill, JBS, and Marfrig. JBS and Marfrig are both Brazilian firms.

Have the packers always been this powerful?

We saw the concentration levels increase through the 1990s. And in fact, up until then, the U.S. Department of Agriculture described ongoing mergers and acquisitions as “merger mania.” And once these firms had reached the current level of concentration, which they've maintained, they've been able to exercise considerable market power. As a result, we see this dysfunctional marketplace and we have alleged that these four meatpackers have conspired in order to artificially depress prices.

We filed a lawsuit in April of 2019, alleging that they have violated US antitrust laws, the Packers and Stockyards Act, and the Commodities Exchange Act. (The lawsuit was dismissed on technical grounds late last year.)

How did the packers conspire to reduce prices?

We allege that they reduced their purchases in the competitive cash market. And we allege that when they do make purchases in the competitive cash market, they essentially work together in order to ensure that cattle prices do not increase.

Can you talk a little bit about how markets for cattle work?

These feedlots across the United States will put their harvest ready cattle on what is called a show list, and they will share this list with all the packers and then they will wait until the packer calls them. Then the packer will say they are interested in purchasing and offer a bid for some or all of those cattle. That's essentially how it works for about 20% of the available cattle.

Meatpackers have all of the rest of their needs, committed to them through some type of captive supply arrangement, either what are called formula contracts, or other alternative marketing arrangements or forward contracts. And so the problem with the industry is there is insufficient competition in the cattle selling process between the independent feeder and the meatpacker.

Why would a cattle rancher sign a captive supply contract?

When you have four packers controlling 85% of the market, they effectively control access to the market. And they can prevent an independent feeder who has cattle to sell from timely accessing the market. So they create market access risk for cattle feeders. And then they solve the problem for the feeder by saying we will guarantee timely access to the market, so long as you enter one of these captive supply contracts.

And even though it doesn't contain a price, the packers base that price somewhere around where the average price discovery point is reached in the competitive cash market. And so you have approximately 80% of the cattle being priced off of this ultra thin cash market. That lowers the price of all the cattle that the packers acquire.

How do they control access to the market? If you're a cattle feeder, what can a packer threaten you with?

Well, they simply won't offer a bid for the cattle and we saw this in March of 2020. Domestic cattle producers could not get a bid from any of the major packers in the United States for many weeks, some up to seven weeks, at the same time that the packers were importing cattle from Canada directly for slaughter. And so they were substituting Canadian cattle for U.S. cattle and essentially depriving the American cattle producer of access to their own domestic market.

Fed animals are perishable commodities, they must be sold within about a three-week window, or they degrade in quality. At some point, the cattle producers’ cost of feeding is no longer economical. So the packers have the ability to force the cattle producer to enter into these otherwise non-competitive contracts simply by denying them access to the marketplace.

Were the Canadian cattle cheaper?

Sometimes Canadian cattle are cheaper than U.S. cattle, though not always.

Why shouldn’t packers just buy the cheaper Canadian cattle?

Well, as we alleged in our lawsuit, they've actually been importing those cheaper cattle uneconomically because of the additional transportation costs of bringing those to the processing plant. And we argue that the packers gain an advantage from that because they can satisfy immediate demand and not cause domestic prices to rally or respond favorably to the increased demand.

Did this dysfunctional market lead to any beef shortages during the pandemic?

In March of 2020, for the first time in memory, consumers went to the grocery store and couldn't buy beef. And it wasn't that we didn't have enough cattle to produce the beef that consumers wanted; the distribution system and the market system completely broke down. So consumers began to looking for alternatives, such as farmers and ranchers who could actually sell beef directly to consumers.

This was a wake up call for America. We have so skeletonized the entire live cattle and beef supply chains that they are no longer capable of withstanding a shock, whether it be the covid pandemic or a climatic circumstance. The industry is incapable of meeting our national food security needs.

What about supermarket consolidation? Is that putting pressure on the industry?

I don't have enough information. I know we have considerable consolidation in the retail sector. But that has not been my focus of analysis.

Walmart has vertically integrated into dairy production. Do you think they might vertically integrate into meatpacking?

I believe they're doing that right now. Walmart has partnered with Creekstone Farms, and that would be the vertical integration model that has now been initiated in the cattle industry.

And what do you think about that? Is that adding a new competitor? Or is that a problem?

It will be the death knell for the American family farm and ranch system of agriculture that has been the envy of the world until recently.

The strength of our system lies in the fact that it consists of disaggregated livestock producers all across America, and regional and local meat processing plants and distribution systems. It was an unprecedented network that ensured that consumers would never go to the grocery store and not have beef on the shelves.

But we are moving in the opposite direction.

We're moving into an industrialized model that has already been perfected in the poultry and hog industries. And you'll recall during the pandemic, that in those two industries they had to euthanize hogs and poultry because the system could not respond to the market shocks.

We have got to change direction from that which we're going and we should disallow any of these types of vertically integrated mergers that will effectively reduce opportunities or independent cattle farmers and ranchers all across America.

Who regulates the cash markets for cattle?

Well, the Packers and Stockyards act of 1921 was intended to protect and preserve competition in the industry, and to protect the actual livestock producer from any unfair, deceptive or unjustly discriminatory practice or conduct by the packers. The problem has been for 100 years that that statute has collected dust. The US Department of Agriculture has chosen not to properly enforce that. In addition, the Justice Department along with Department of Agriculture has chosen not to properly enforced our antitrust laws. And so that has led us to where we are today, with a disinclination by regulators to actually enforce existing statutes.

Well, but it does seem like there's a distinction. If it's a 100 year old problem, you would have seen consolidation in the 1920s and 1930s. And there wouldn't be any family owned ranchers. But that's not the case. So something happened, it sounds like the merger wave in the 90s has changed that dynamic.

Before the Packers and Stockyards Act was passed in Congress, the meatpackers entered into a consent decree with the Department of Justice. And they essentially agreed that they would not own and control feedlots within the sector. And that changed in the 1980s, through the deregulation era that we experienced. And that's what prompted the mergers and acquisitions wave. And from that point forward, the packers began the process of vertical integration. So it has been a relatively new phenomenon that has occurred, at least since the 80s.

What was the specific policy in the 80s that allowed for that vertical integration?

One example is that the Packers and Stockyards Administration had a regulation that prohibited the packers from custom feeding cattle. That regulation was rescinded. So that was one of the measures that essentially unleashed the packers’ ability to do as they please within the industry.

[Matt Stoller comments: Packers being able to custom feed cattle is a form of vertical integration in which packers begin owning cattle directly. In negotiating with farmers to buy their cattle, packers can use their own cattle as leverage to drive prices down, which is what the Packers and Stockyards administration found happened in the 1960s.]

Got it. And then in the 90s, there was this consolidation, to take advantage of that, but also just to consolidate. What do we do about this problem?

Because of the acute dysfunction that we're currently facing, we must do triage. First we need to restore competition for beef that is produced by US cattle producers. By doing this, we can address the fact that we're importing 3 billion pounds of beef from 20 different countries. And that beef is a direct substitute for US beef because it is undifferentiated in the marketplace. The consumer doesn't know if they're buying from Argentina or Uruguay or Namibia, or if they're buying beef produced by the American cattle producer. So we must establish competition for USDA beef. And the way to do that is for Congress to pass a mandatory country of origin labeling for beef, so all beef sold in America is labeled as to where it was born, raised and slaughtered.

The second step we need to do is to reinject competitive forces into the cattle market itself. There’s a Senate bill introduced by Senators Chuck Grassley and Jon Tester that would require the packers to purchase at least 50% of their weekly cattle needs from the cash market instead of relying on captive supply. The packers have got to be forced to purchase their cattle in that market.

Once those two steps are taken, then we need to look longer term. We need to ban the packers ability to own and control cattle long before harvest. In other words, we need to stop the vertical integration of the industry. And we need to prohibit these unpriced contracts, these contracts that give the packers considerable market leverage, because they have their supply needs committed to them without having to purchase them in a competitive marketplace.

No vertical integration is kind of like a Glass-Steagall type of arrangement. You can't process the cattle and own the cattle.

Packers should be packers and cattle producers should be cattle producers, but packers should not also be cattle producers.

That's actually similar to Amazon being the marketplace and selling through the marketplace. What about breaking up the packers?

We have two choices in terms of ensuring competition in the marketplace, you know, you would either break them up or you would regulate them to ensure that they do not interfere with competitive forces. So we do have two choices there. But the fact that the supply chain and the distribution chain is broken indicates that we need far more local and regional meatpacking processors, and a new distribution system as compared to what we have. So we are supporting, for example, the ability of smaller packers to begin selling beef interstate across state lines where they have been prohibited from doing so up until now. And so we must rethink the entire live cattle supply chain and beef supply chain in order to attain a level of national food security that Americans deserve.

You're not saying we should break up packers. But you're saying we need more diversity of packers. And if breakups lead to that then great. If not, let's find another way to do it.

Yes.

Anything else you want to tell me?

I think you've got it covered.

If you’d like to sign up to receive issues over email, you can do so here. Thanks to Todd Mentch for copy-editing.

I operate a small publication and once tried to produce a text interview with members of the Chicago Symphony Orchestra about their strike in the spring of 2019. It was a disaster and never made it to print because I could not afford the labor involved in transcription and editing. This interview was very interesting, especially for someone looking to purchase and operate a small farm, as I am, but it is littered with textual errors. I know you have said on previous occasions that you err on the side of promulgating ideas despite minor defects, which is sensible. This is not at all an easy problem to solve, but this is exactly the type of content that could comprise the paid supplement to your newsletter, and perhaps the additional revenue could be invested in additional editorial capacity. I purchased Goliath and have been reading it assiduously in the hopes that I can better participate in the discussions here. Keep up the good work!

Interesting, although hard to get my head round how the captive non cash contracts work.

It does make think think cattle ranchers should just team up with start up meat packers and distribute to local stores,supermarkets and restaurants